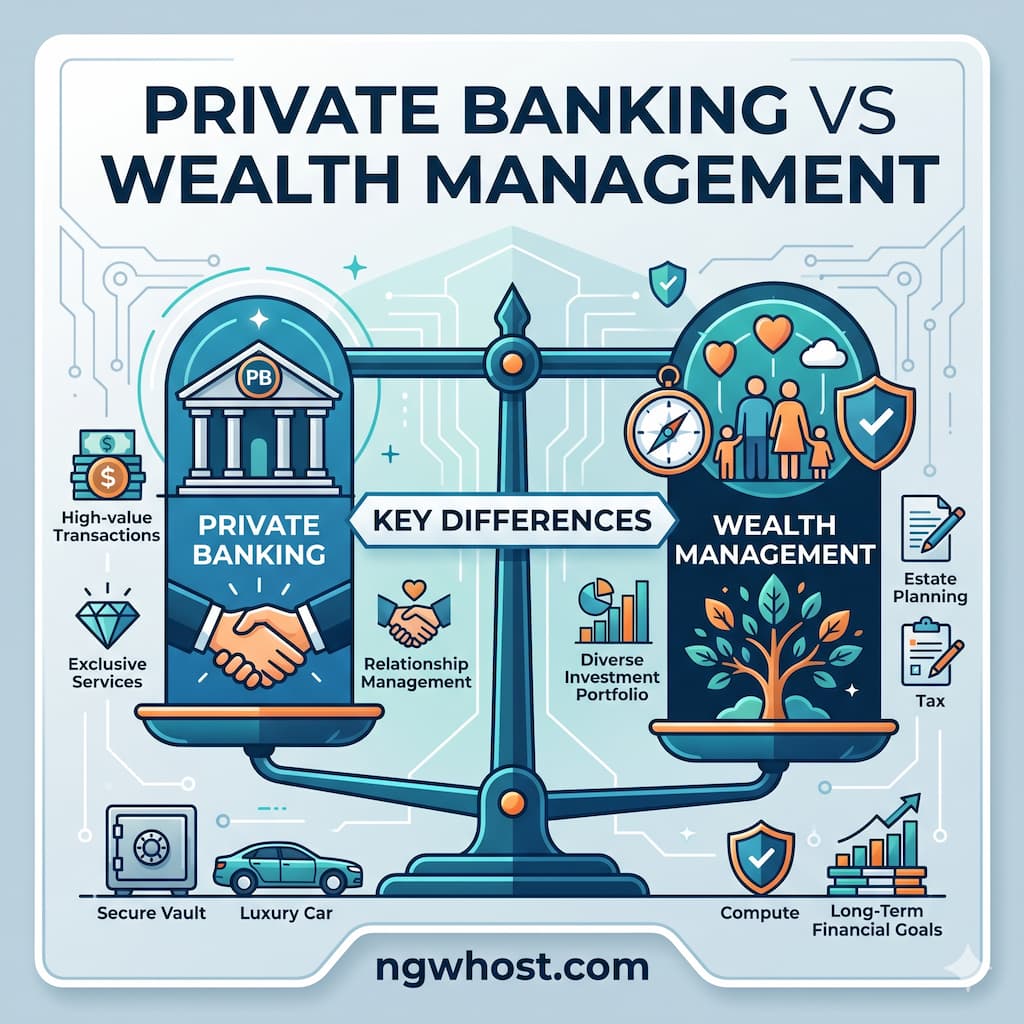

Private Banking vs Wealth Management: Key Differences

In the sophisticated financial landscape of 2026, the terms “Private Banking” and “Wealth Management” are often used interchangeably by the general public. However, for the high-net-worth individuals and entrepreneurs who frequent ngwhost.com, understanding the surgical distinctions between these two services is the difference between simply storing money and strategically multiplying it.

As global markets face new challenges—ranging from AI-driven volatility to shifting tax regulations—the way you manage your capital must be more precise than ever. While both services cater to affluent clients, they operate with different philosophies, toolsets, and end goals. This comprehensive guide breaks down the structural, functional, and strategic differences to help you decide which path aligns with your financial future.

1. Defining the Core Philosophies

To understand the difference, we must look at the primary objective of each service.

What is Private Banking?

At its heart, Private Banking is a personalized branch of retail banking. It is built on the foundation of banking services and exclusivity. If you are a private banking client, you are assigned a dedicated relationship manager who acts as your “concierge” to the bank’s entire ecosystem.

- The Focus: Liquidity, credit, and high-end banking transactions.

- The Vibe: High-touch, personalized service that simplifies your daily financial life.

What is Wealth Management?

Wealth Management is a much broader, more holistic discipline. It is not necessarily tied to a specific bank. Instead, it focuses on the total optimization of a client’s financial life. A wealth manager looks at your assets, your liabilities, your taxes, and your legacy.

- The Focus: Investment strategy, asset allocation, and long-term financial planning.

- The Vibe: Strategic, advisory, and focused on the “big picture” of wealth preservation and growth.

2. Service Offerings: Concierge vs. Consultant

The actual “menu” of services provided by each professional is where the paths truly diverge.

The Private Banking Suite

Private banking is about providing specialized access to traditional banking products:

- Custom Credit Solutions: Need a multi-million dollar mortgage for a vacation home or a bridge loan for a business acquisition? Private banks offer flexible terms that standard retail branches cannot.

- Preferential Rates: Higher interest on savings and lower interest on debt.

- Currency Management: In 2026, managing multi-currency accounts and international transfers is a cornerstone of private banking for global citizens.

- Lifestyle Services: Access to exclusive events, airport lounges, and concierge services that go beyond finance.

The Wealth Management Suite

Wealth management is about the “Science of Capital.” The services are more consultative:

- Asset Allocation: Diversifying across stocks, bonds, real estate, and private equity.

- Tax Optimization: Working with accountants to ensure your investment structures are tax-efficient (crucial in the shifting regulatory environment of 2026).

- Estate and Succession Planning: Managing how wealth is transferred to the next generation or philanthropic causes.

- Retirement Planning: Calculating cash flow requirements for decades into the future.

3. The Minimum Entry Requirement: The “Threshold”

In 2026, the barriers to entry for these services have evolved, but they remain a key differentiator.

| Feature | Private Banking | Wealth Management |

| Minimum Assets | Usually $250k – $1M in liquid cash. | Usually $1M+ in investable assets. |

| Focus Area | Deposits, Loans, and Cash Flow. | Portfolios, Taxes, and Estate. |

| Provider | Large Commercial Banks. | Independent Firms or Specialized Units. |

| Relationship | Relationship Manager (Banker). | Wealth Advisor (Consultant). |

Note: Many “Full-Service” firms now offer both, but the entry point for the high-end wealth advisory side is typically higher than the banking side.

4. Investment Philosophies: Execution vs. Strategy

How your money is actually put to work differs significantly between these two models.

Private Banking: Product-Centric

Private banks often have a list of “in-house” investment products. While they provide excellent execution, their suggestions may lean toward the bank’s own mutual funds or structured products. It is an execution-heavy model.

Wealth Management: Strategy-Centric

Modern wealth management in 2026 is increasingly “fiduciary-first.” This means the advisor is legally obligated to act in your best interest. They use an Open Architecture approach, meaning they can pick the best stocks, ETFs, or alternative investments from anywhere in the world, regardless of which bank holds the assets.

5. The Impact of AI in 2026

Both sectors have been revolutionized by Artificial Intelligence, but in different ways.

- In Private Banking: AI is used for frictionless service. Chatbots handle routine transfers, and predictive models anticipate when you might need a new line of credit or a currency hedge.

- In Wealth Management: AI is used for Hyper-Personalized Alpha. Wealth managers use AI to run “Monte Carlo simulations” that predict how your portfolio will perform under 10,000 different economic scenarios, including potential 2026 market shocks.

6. Fee Structures: Transparent vs. Transactional

At ngwhost.com, we always tell our readers: Follow the money. Understanding how your advisor gets paid tells you where their loyalty lies.

Private Banking Fees

Fees are often “bundled” or based on transactions. You might pay for the specific loans you take out, or the bank earns a spread on the products you buy. Some banks offer “Free” private banking if you maintain a high enough balance (because they make money on your deposits).

Wealth Management Fees

Wealth managers typically charge a percentage of Assets Under Management (AUM), usually ranging from 0.5% to 1.5%.

- The Alignment: This model aligns their success with yours. If your portfolio grows, their fee grows. If your portfolio shrinks, they take a pay cut.

7. Which One is Right for You?

Choosing between the two depends on your current “Financial Phase.”

Choose Private Banking if:

- You have high cash flow and need sophisticated credit solutions.

- You travel internationally and need seamless multi-currency support.

- You value personal, “white-glove” service for your daily banking needs.

- Your wealth is currently “simple” (mostly cash and high income).

Choose Wealth Management if:

- You have a large amount of capital that needs a long-term growth strategy.

- Your tax situation is becoming complex (multiple income streams, international assets).

- You are thinking about your legacy and how to pass wealth to your children.

- You want an advisor who looks at your entire balance sheet, not just your bank account.

8. The 2026 Hybrid Approach

For many entrepreneurs, the answer is not “either/or” but “both.” In 2026, the most successful individuals use a large bank for their Private Banking (for the credit lines and the global debit cards) but hire an independent firm for their Wealth Management (to ensure unbiased investment advice and tax planning). This creates a system of checks and balances that protects your capital from institutional bias.

Read More⚡ Emerging Markets 2026: The Best Opportunities Now

Conclusion: Mastering Your Capital

Wealth is more than a number; it is a tool for freedom. Whether you choose the personalized convenience of Private Banking or the strategic depth of Wealth Management, the goal remains the same: to ensure your money is working as hard for you as you did to earn it.

At ngwhost.com, we believe that the informed investor is the most successful one. By understanding the differences between these two pillars of finance, you can build a support team that doesn’t just manage your money, but secures your future.

The markets of 2026 are fast and unforgiving. Make sure you have the right partner in your corner.